How to Prepare for the End of the Tax Year

Updated 16 Mar 2026

Written by

Categories

Each April, the UK tax year resets, and with it, a fresh set of allowances and reliefs that are simply lost if left unused.

As the 5th April 2026 deadline for the 2025/26 tax year approaches, now is the time to take stock of what remains available to you so that you can make sure that your wealth is working as efficiently as possible.

It’s time to think about your pensions and ISAs and join the many UK individuals reducing their tax bill efficiently

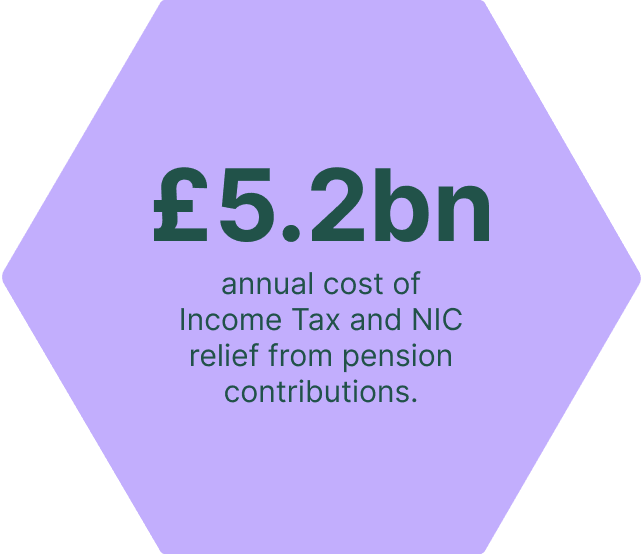

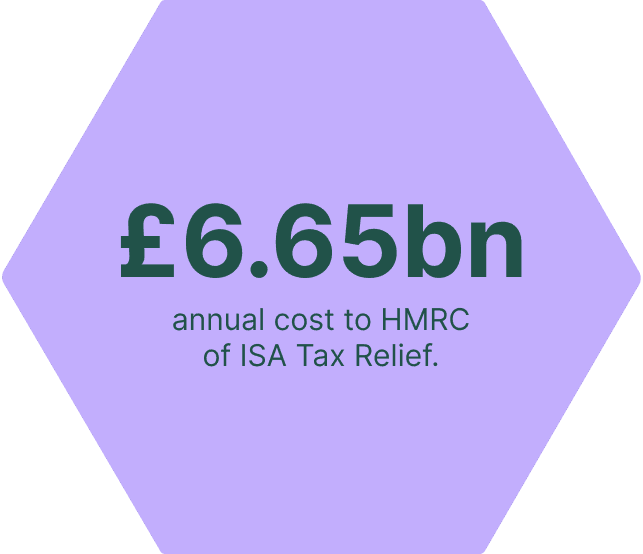

Source: As reported by HMRC in relation to the 2023/24 Tax year.

Claiming your share doesn't require complex strategies; just straightforward planning and making full use of the allowances you are entitled to.

How Pension Contributions Help You Save Tax

The government offers tax relief on pension contributions to incentivise you to save money for retirement.

Tax Relief on Personal Pension Contributions

If you are making personal pension contributions, as long as you’re a UK resident under the age of 75, HMRC will add 20% basic-rate tax relief to your net contribution.

Generally, you can invest as much as you earn up to £60,000 each tax year and get tax relief. Even if you have little or no income, you can still contribute up to £3,600 gross into a pension and receive tax relief. It is worth noting that a reduced tapered annual allowance may apply if your income exceeds certain thresholds.

If you pay a higher rate than 20%, then you could claim significant further relief on your self-assessment return.

Employer Pension Contributions and Corporation Tax Benefits

Pension contributions also offer significant opportunities for business owners and company directors to make contributions through their limited companies.

Investing money from a UK company into a pension scheme is treated as a deductible expense for corporation tax purposes. This means the full contribution reaches the pension without the amount you invest being reduced by tax leakage.

Your ISA Allowance Explained

You can invest up to £20,000 each tax year using your ISA allowance, giving you access to several valuable tax advantages:

- By moving cash holdings into an ISA, the interest your cash generates is free of any tax.

- If you choose to invest through a Stocks and Shares ISA, any interest, dividends, or capital gains are completely free from tax.

Your allowance can be spread across different ISA types to suit different objectives. You can choose from:

- Cash ISAs for short-term certainty

- Stocks and Shares ISAs for longer-term growth

- Lifetime ISAs for first home or later-life planning (within the £4,000 annual LISA limit)

Using the allowance strategically can ensure each part of your investment strategy is aligned with its purpose, your circumstances, and time horizon.

For children, up to £9,000 can be invested into a Junior ISA each tax year, and this is separate from the adult £20,000 ISA limit. You can also contribute to a child’s pension. It’s never too early to plan for retirement!

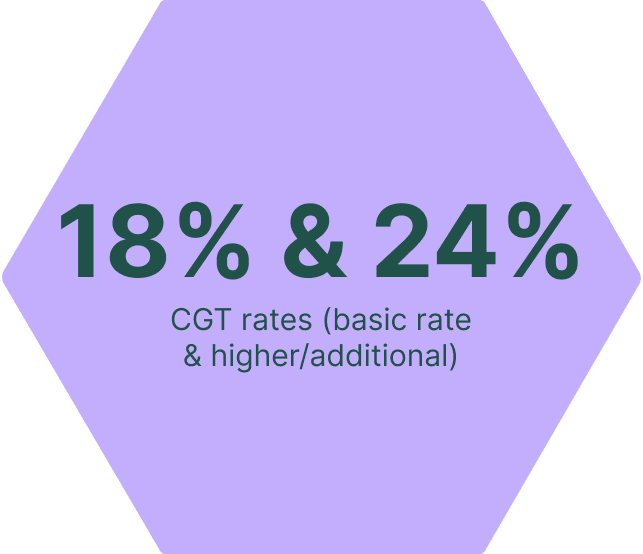

How to Use Your Capital Gains Tax Allowance

Capital Gains Tax (CGT) is paid on any profits you make when you sell or dispose of an asset that has increased in value.

If you already hold investments outside of a tax wrapper, you could consider moving them into a more tax-efficient account like an ISA or pension, as outlined above.

It is worth remembering that doing so may involve selling existing holdings, which could trigger a CGT liability. This allows future growth and income to be sheltered from CGT.

You might also consider deliberately crystallising gains up to your £3,000 capital gains tax allowance before the end of the tax year. This allowance cannot be carried forward, so if you don’t use it by 5th April, you lose it.

How Couples and Families Can Use Tax Allowances

If you have already used your own allowances, you could consider paying into an ISA or pension on behalf of a loved one. This could be a child, spouse, or civil partner, and importantly, saving into someone else’s account does not affect how much you can save into your own.

Spousal transfers also benefit from being able to share assets and allowances for tax purposes. You can usually transfer investments without having to pay CGT at that point.

Between a married couple, for example, you could also together realise gains of up to £6,000 in the current tax year without paying any capital gains tax. Assuming that both individuals own the relevant assets and neither has used their annual exempt amount elsewhere.

You can also use the marriage allowance if one of you is a non taxpayer and the other is a basic-rate taxpayer. This allows a transfer of £1,260 of the former’s personal allowance to their spouse, creating a potential tax saving of up to £252 per year.

The marriage allowance is straightforward to set up. If your circumstances fit, it’s an easy win. However, this will only apply where one partner has unused personal allowance and the other pays tax at the basic rate only.

Next Steps Before the End of the Tax Year

With less than a month until the end of the 2025/26 tax year, now is the perfect time to make sure you're set to begin the next tax year.

This involves maximising your allowances where appropriate, reviewing available reliefs and asset allocations as part of your tax-efficient financial planning.

If you'd like to discuss how to make the most of your remaining allowances before 5th April, get in touch with our team.

This article is for general information purposes only and does not constitute financial, tax, or investment advice. It should not be relied upon as a basis for making financial decisions. Tax treatment depends on individual circumstances and may be subject to change in the future. The value of investments can go down as well as up, and you may get back less than you invest. Past performance is not a reliable indicator of future results. Aventur Wealth Limited is not a firm of accountants or tax advisers. We recommend you seek independent tax advice where appropriate.

MORE LIKE THIS

See all

8 December 2025

Autumn Budget 2025: What does it Mean for Your Money?

17 November 2025

Autumn Budget 2025 Key Predictions

14 March 2025

How to Prepare for the End of the Tax Year

1 November 2024

Autumn Budget Key Points: How Will your Finances be Affected?

16 October 2024

Autumn Budget 2024 Predictions

11 September 2024

Maximising Your Retirement: A Guide to Pension Contributions and Tax Benefits

20 March 2024

How to Prepare for the End of the Tax Year

18 March 2024

Spring Budget 2024 Key Points

16 August 2023

Inheritance Tax: What You Need to Know